|

|

|

The types of insurance are: An example is the Mortgage Reducing Term Assurance which is a cover for the cost of house purchased i.e. the balance of the housing loan will be fully settled by the insurance company in the event of death or permanent disability of the purchaser.

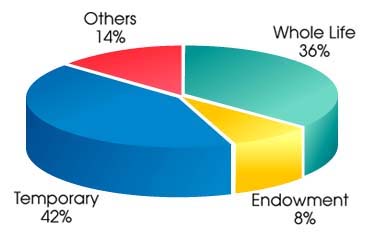

The more popular endowment policies are for education purposes, whereby the parent wants to protect his child's education fund. Chart 1 1994 - Distribution of New Sums Insured Source: Annual Report of the Director General of Insurance 1995 As an illustration of a whole of life insurance cover we take a young executive aged 26: Salary : RM2,000 x 12 = 24,000 per annum The executive takes up a whole of life policy of RM100,000. Monthly premium is approximately RM200. Since the insurance company pays out cash bonus on the premiums paid, premium payments can be paid via the bonuses and therefore can effectively be stopped after several years. The cover will go on until the executive turns 65 years old if no claims are made. From a savings point of view, after 29 years i.e. executive is now 55 years old and having paid RM33,600 in premiums, the cash value of the policy would be about RM80,000 which can be withdrawn and used as a retirement benefit. The return is approximately 4.8% which is about the same as the savings rate. If he stretches it out until the turns 65, the cash value is about RM134,000. The return of 7.7% here is equal or even better than fixed deposits. From a coverage point of view, if the executive dies at the age of 50, his next of kin will receive a death benefit of about RM216,000. The same amount will be paid out if he suffers from a stroke and becomes permanently disabled, which can be useful in taking care of medical costs that has exceeded his employer's limit. It is reported that Bank Negara will pursue vigorous policy initiatives to quickly develop the insurance sector as a key component of the financial services sector. One of the targets of the insurance industry by the year 2000 is that one in every two persons should hold a life policy. As can be seen from the above illustration, insurance is a must to protect your family in case something unexpected happens. It is a vital part in financial planning. For most of us, it is wise to have insurance cover and invest the balance of the funds in other savings plans that are available in the market. Adopting this course of action (insurance and other savings plans) will result in, you as the investor being able to have your cake and eat it. Something we don't have an opportunity to do often.

|

|||